India’s cement sector is set to welcome a new major listing – JSW Cement Limited. Backed by the JSW Group, the IPO has generated buzz among retail and institutional investors, thanks to the company’s strong green cement credentials and ambitious expansion plans.

What is JSW Cement IPO listing date?

The listing date for the JSW Cement IPO is Thursday, August 14, 2025, when the shares will debut on both the National Stock Exchange (NSE) and the Bombay Stock Exchange (BSE). Before you commence active trading wef August 14, let us understand overview of this IPO.

1. Overview & Structure

- IPO Size: ₹3,600 crore total – comprising a ₹1,600 crore fresh issue and a ₹2,000 crore offer for sale (OFS) by existing shareholders.

- Price Band: Priced between ₹139 and ₹147 per share.

- Allotment of Shares in OFS:

- Apollo Management (via AP Asia Opportunistic Holdings Pte Ltd) – ₹931.8 crore worth of shares.

- Synergy Metals Investments – ₹938.5 crore.

- State Bank of India – ₹129.7 crore.

- Investor Allocation:

- QIBs (Qualified Institutional Buyers): 50%

- NIIs (Non Institutional Investors): 15%

- Retail Investors: At least 35%

2. Purpose & Use of Funds

- Capacity Expansion: ₹800 crore allocated for a new integrated cement plant in Nagaur, Rajasthan.

- Debt Reduction: ₹520 crore intended for repayment or prepayment of existing borrowings.

- General Corporate Purposes: The remaining roughly ₹280 crore is set aside for other operational expenses.

3. Operational & Financial Snapshot

- Capacity & Coverage: As of March 2025, JSW Cement had a grinding capacity of 20.6 MMTPA and clinker capacity of around 6.44 MMTPA, with seven plants across South, West and East India and one in the UAE.

- Green Credentials:

- Largest producer of GGBS in India with 84% market share.

- Maintains the lowest CO₂ emission intensity among Indian peers.

- High use of waste – derived inputs and green power.

- Financials:

- FY24 Revenue: ₹6,028 crore with a net profit of ₹62 crore.

- FY25 Revenue: Slight dip to ₹5,914.7–₹5,913 crore and a net loss of ₹163.7 crore.

4. IPO Subscription & Market Sentiment

- Day 1 – 2: Subscription crossed 30% with steady interest from institutions.

- Day 3: Fully subscribed, ending with 7.7x overall subscription.

- GMP (Grey Market Premium): Initially surged to ₹20 – 21 (13% premium) after price band news, later stabilised around ₹2 – 4 (1–3% premium).

Analysts have given a “Subscribe” rating, especially for long term investors who believe in the cement sector growth story.

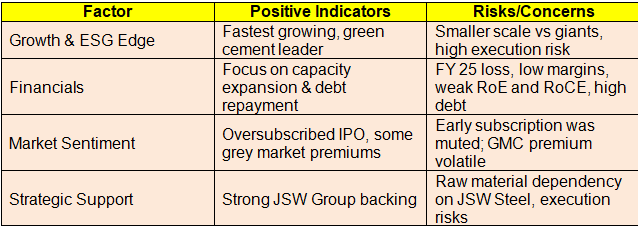

Why should you invest in JSW cement share?

Certain positive factors favouring why you should invest in JSW cement stock and risks associated with it are tabulated as below:-

Is it good time to invest in cement stocks now?

Right now, there are several structural, cyclical and policy driven factors making the cement sector in India look promising – especially if you have a medium to long term horizon.

- Government’s Big Infrastructure Push

- National Infrastructure Pipeline (NIP) and PM GatiShakti are driving massive investments in highways, bridges, ports and urban infrastructure.

- Union Budget 2025 again increased capital expenditure on infra by double digits, which directly fuels cement demand.

- Affordable housing schemes like PM Awas Yojana (Urban & Rural) are being scaled up – cement is a core beneficiary.

2. Real Estate Recovery & Urbanisation

- Post pandemic, residential and commercial real estate demand has rebounded strongly in Tier 1 and Tier 2 cities.

- Large developers (DLF, Godrej, Prestige) have record project pipelines, boosting cement offtake.

- Urbanisation rate is expected to rise from 36% today to 40% by 2030, creating sustained construction needs.

3. Rural Demand Revival

- Rural infrastructure projects (roads, irrigation, schools, health centres) are expanding.

- A good monsoon cycle typically increases rural housing construction – which is cement intensive.

4. Dynamics Turning Favourable

- Capacity Utilisation Rising: From 65-70% in 2022 to 75–80% now – stronger pricing power.

- Consolidation Trend: Big players (UltraTech, Adani, Shree, JSW) are acquiring smaller units, leading to better efficiency and cost control.

- Green & Blended Cement Growth: Companies focusing on low clinker, low carbon products (like JSW’s GGBS) are tapping ESG driven demand.

5. Cost Pressures Easing

- Pet Coke and Coal Prices have softened from the peaks of 2022–23, improving margins.

- Freight cost stability (with diesel price moderation) supports profitability.

6. Long Term India Story

- Per capita cement consumption in India is 250 – 275 kg, far below China’s 1,600 kg – huge room to grow.

- IMF & RBI still project India as one of the fastest growing large economies – cement will ride that wave.

Investment View

- Short Term: Likely benefit from strong infra spending and real estate launches in FY26.

- Medium Term (3-5 years): Rising per capita consumption + industry consolidation = stable margins + volume growth.

- Risks: Cyclical nature (demand slowdown in weak economy), fuel price volatility, policy changes in infra spending.

Bottom line

If you believe India’s infra and housing boom is just getting started, the cement sector is a direct play on that growth. The best approach could be a mix of leaders for stability (UltraTech, Shree Cement, Ambuja) and emerging growth players (JSW Cement, Dalmia Bharat, Ramco) for higher returns – balancing safety and upside.